{kind=link}

The narrow strip of water separating Iran from the Oman Peninsula — barely 33 kilometers wide at its narrowest point — has long been considered the world’s most critical maritime chokepoint. The Strait of Hormuz does not merely carry oil. It carries civilization’s modern industrial metabolism: the energy that powers factories, the feedstocks that become plastics, the fuels that move goods across oceans. When that artery closes, the consequences ripple outward in cascading waves, touching nearly every sector of the global economy. But few industries feel the pain as acutely, or as quickly, as the packaging supply chain — a vast, interconnected system that underpins everything from food safety and pharmaceutical distribution to e-commerce logistics and consumer goods retail.

1. The Strait in Numbers

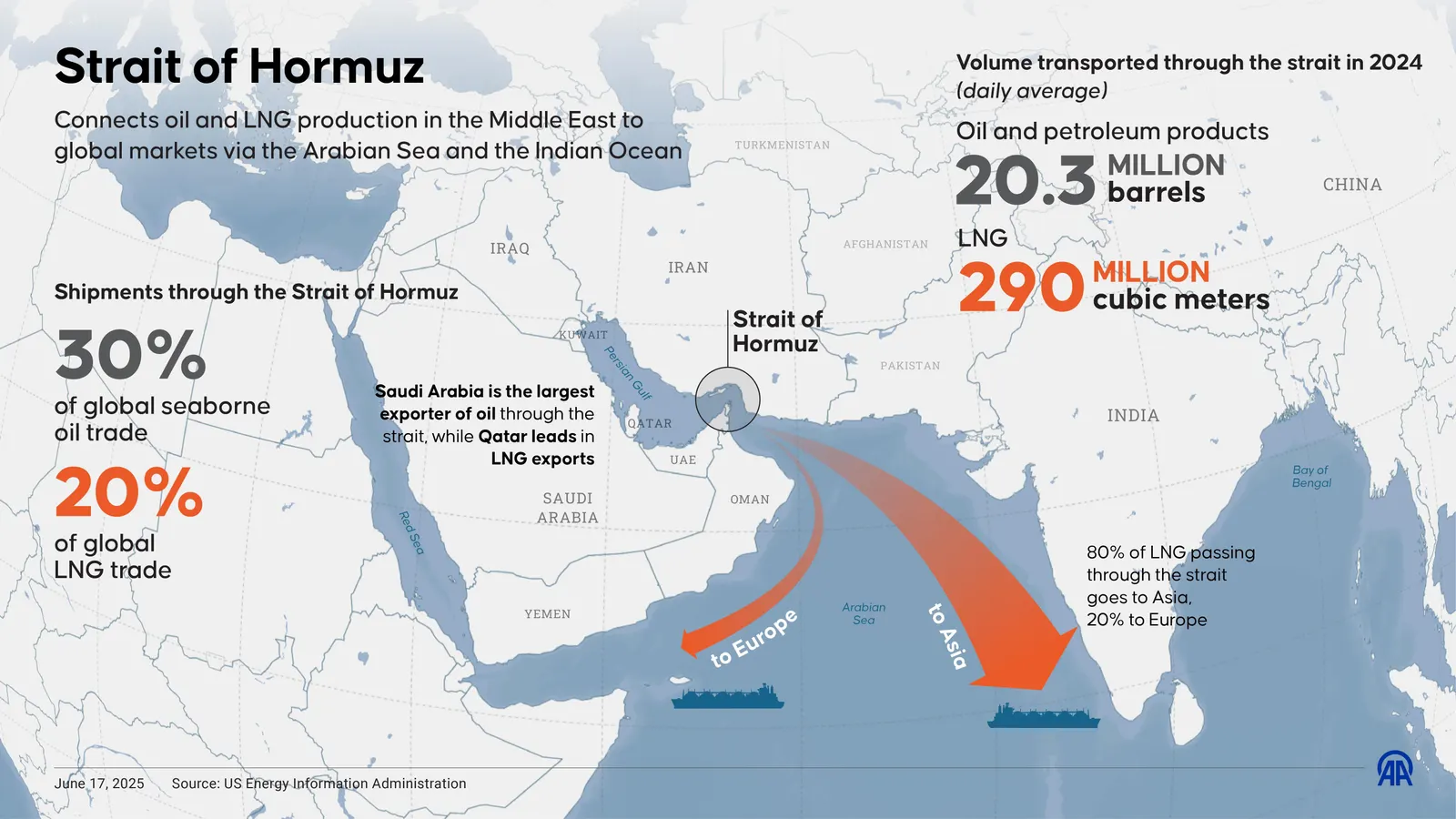

To understand the scope of disruption, one must first appreciate what the Strait of Hormuz actually carries. In 2025, approximately 13 million barrels per day of crude oil transited the waterway, representing roughly 31% of all seaborne crude oil flows globally. Beyond crude, the strait handles approximately 22% of global liquefied natural gas (LNG) trade, channeling supplies from Qatar — the world’s largest LNG exporter — and the UAE to buyers across Asia, Europe, and beyond.

Major producing nations that rely on the Strait for their export revenues include Saudi Arabia, Iraq, Iran, Kuwait, the UAE, and Qatar. For most of these countries, the Strait is not an option — it is the only viable maritime export corridor. Saudi Arabia has partially mitigated this exposure with the East-West Pipeline (Petroline), which can carry up to 5 million barrels per day to Red Sea terminals. The UAE has its own Abu Dhabi Crude Oil Pipeline (ADCOP), capable of moving roughly 1.5 million barrels per day to Fujairah, bypassing Hormuz entirely. But combined, these pipelines can offset only a fraction of the roughly 13 million barrels per day that normally transit the Strait. For LNG, there is no pipeline alternative whatsoever — all Qatari and UAE gas exports that don’t travel by sea simply don’t travel.

Analysts at JPMorgan Chase estimate that a halt in Hormuz lasting 25 days would fill producer nations’ storage tanks to capacity, forcing them to cut production. Under a prolonged closure scenario, oil prices rising above $100 per barrel become “increasingly plausible,” according to Middle East Briefing, while CNBC’s energy desk has noted that some analysts see the potential for crude prices to match or exceed the 2008 oil shock.

For packaging professionals, these headline numbers matter enormously. The packaging supply chain is one of the most oil-intensive industries in the modern economy, not simply because it uses energy to operate, but because petroleum is the foundational raw material from which most packaging substrates are made.

2. The Petrochemical Backbone of Packaging

Modern packaging is, in a very real sense, bottled oil. The majority of flexible and rigid plastic packaging materials — polyethylene (PE), polypropylene (PP), polyethylene terephthalate (PET), polystyrene (PS), and polyvinyl chloride (PVC) — are derived from petrochemical feedstocks, primarily ethylene and propylene, both of which are cracked from crude oil-derived naphtha or natural gas liquids. These polymers form the building blocks of stretch film, shrink wrap, pouches, bottles, trays, caps, closures, laminates, and countless other packaging formats used across food, beverage, personal care, pharmaceutical, and industrial applications.

The relationship between crude oil prices and polymer pricing is well-established and largely mechanical. When crude rises, naphtha becomes more expensive. When naphtha rises, ethylene and propylene cracking becomes costlier. When those olefins spike, PE and PP resin prices follow suit. The global petrochemical market, valued at approximately $743.5 billion in 2026, is built on this price transmission chain, and the packaging sector sits at the downstream end, absorbing whatever shocks originate in oil markets.

Ethylene, the key building block for PE, and propylene, the feedstock for PP, are produced predominantly through steam cracking in large, energy-intensive complexes — many of which are located in the Middle East precisely because of the region’s cheap and abundant feedstock access. The Gulf Cooperation Council (GCC) region, including Saudi Arabia, the UAE, Qatar, and Kuwait, has become one of the world’s largest petrochemical production hubs over the past three decades, supplying polymer resins to packaging manufacturers globally, particularly in Asia and Europe.

A closure of the Strait of Hormuz does not merely raise oil prices. It physically interrupts the movement of petrochemical feedstocks and finished resins from their source to their buyers. Ethylene, propylene, benzene, and a range of polymer pellets are routinely shipped through Hormuz aboard petrochemical tankers and bulk carriers. When the waterway closes, these flows stop — and no amount of pipeline substitution can fully compensate. The packaging supply chain faces not just higher input costs, but potential feedstock shortages that cannot be resolved by paying more.

3. Plastic Packaging: A Dual Price Shock

The impact on plastic packaging unfolds through two simultaneous channels: a feedstock cost shock and an energy cost shock.

On the feedstock side, naphtha — the most common olefin cracking feedstock in Asia and Europe — is directly priced against crude oil. A jump to $100 per barrel crude translates almost immediately into naphtha prices above $700 per metric ton, a level that crushes the margins of cracking complexes already operating near break-even. As S&P Global Commodity Insights noted, “naphtha and ethylene margins are already in the negatives” even before the current crisis. A sharp crude spike on top of an already stressed margin environment risks forcing curtailments at cracking facilities, tightening the supply of ethylene and propylene and pushing polymer resin prices sharply higher.

On the energy side, plastics manufacturing is extraordinarily energy-intensive. Polymerization reactors, extruders, injection molding machines, thermoforming equipment, and blown film lines all consume substantial quantities of electricity and natural gas. Higher energy prices directly inflate manufacturing costs for every packaging converter, whether they operate in Shanghai, Stuttgart, or Sao Paulo. For facilities in Asia — particularly in India, South Korea, Thailand, and the Philippines, all identified by Nomura as among the most vulnerable to the Hormuz closure — the dual shock of costlier feedstock and costlier energy creates an almost unavoidable margin squeeze.

Polypropylene (PP) presents a particularly acute case. Even before the current crisis, PP suppliers had already reduced production rates to below 70% in late 2025 amid a supply-demand imbalance, bringing inventory levels down to just 35 days — well below the 38 to 42-day average of recent years. With so little buffer in the system, any further supply disruption driven by feedstock scarcity or energy-cost-driven curtailments could rapidly translate into physical shortages for packaging converters. PP is used ubiquitously in food packaging trays, caps and closures, flexible pouches, labels, and woven packaging sacks — its scarcity would be felt widely and quickly.

Polyethylene terephthalate (PET), the resin of choice for bottles and clear packaging, faces similar pressures. PET is produced from purified terephthalic acid (PTA) and monoethylene glycol (MEG) — and MEG is a direct ethylene derivative. In the Asian market, where packaging supply chains are concentrated, “polymer price elasticity is increasingly linked to logistics efficiency and port congestion,” and “disruptions in shipping lanes or container availability can rapidly transmit cost increases across resin markets”. The Hormuz disruption delivers both problems simultaneously: feedstock cost shocks and port congestion as vessels are rerouted, trapped, or suspended.

4. Paper and Cardboard: Indirect but Significant Impacts

Plastic is not the only packaging material affected by a Hormuz closure. Paper and cardboard packaging — used extensively in e-commerce, food service, corrugated shipping containers, and retail shelf-ready packaging — faces its own set of disruptions, largely indirect but no less serious.

The pulp and paper industry depends on globally traded raw materials, with major pulp exporters in Brazil, Canada, Sweden, and Finland supplying mills in Asia (particularly China, which produces a substantial share of the world’s paper and paperboard) and Europe. A Hormuz closure adds two to three weeks to voyage times for vessels rerouting via the Cape of Good Hope — the same detour forced on carriers during the Red Sea crisis of 2024. For pulp shipments heading from South America or the Nordic countries to Asian paper mills, these added voyage times mean higher freight costs, delayed deliveries, and the need for larger working capital to buffer the extended pipeline.

Beyond freight, the energy dimension bites the paper sector hard. Pulp and paper manufacturing is one of the most energy-intensive industries in the world. When natural gas and LNG prices spike — as they would in a prolonged Hormuz closure, given that roughly 22% of global LNG trade transits the Strait — operating costs at pulp mills rise sharply. Facilities without long-term energy contracts could face operational curtailments, further tightening pulp supply and pushing up the cost of paper-based packaging substrates.

Chemical inputs are another vulnerability. The paper manufacturing process relies on caustic soda and methanol, among other chemicals, many of which are produced in or exported through the Middle East Gulf. Shortages or price spikes in these chemicals would ripple through the cost structure of every paper mill that sources them from the region, adding yet another layer of inflation to the cost of paper and cardboard packaging.

5. Aluminum and Glass Packaging: The Metal Squeeze

Aluminum packaging — cans, foil, closures, tubes — faces a distinctly material threat from a Hormuz disruption. Aluminum smelting is extraordinarily energy-intensive, requiring vast quantities of electricity, typically generated from natural gas. The Middle East has become a significant producer of primary aluminum precisely because of its cheap energy base; the UAE, Bahrain, and Saudi Arabia are among the region’s key producers, and their output is heavily dependent on natural gas that is either produced locally or imported via LNG.

When Hormuz closes, Middle Eastern aluminum smelters face two threats: higher energy costs if their gas supply is disrupted, and sharply higher logistical costs to export their metal. Fidelity’s analysis of commodity markets notes that “risks to Western aluminium supply rise as Iran war escalates,” and that producers “sitting on the wrong side of the Strait of Hormuz” represent a meaningful supply risk for global buyers. FACE, the European aluminum industry federation, had in fact been warning since mid-2025 about the vulnerability of aluminum supply chains to exactly this kind of geopolitical disruption. War Risk Surcharges from Hapag-Lloyd, set at $1,500 per TEU as of March 2, 2026, add approximately $75 per tonne to the shipping cost of aluminum ingot — a meaningful increment in a market where margins are already thin.

The result for packaging manufacturers that rely on aluminum — can makers, foil laminators, closure manufacturers, flexible packaging converters — is a combination of tighter supply, higher material costs, and the need to seek alternative sources potentially from producers in less geopolitically exposed regions such as Norway, Canada, or Australia. These alternatives exist, but they take time and logistics reorganization to activate, and in the short term, the gap between demand and accessible supply will drive prices higher.

Glass packaging is less directly exposed to Hormuz than plastic or aluminum, since glass is manufactured primarily from silica sand, soda ash, and limestone — materials not linked to oil in the same way. However, glass furnaces require enormous quantities of energy, and natural gas is typically their fuel of choice. As LNG prices spike alongside crude oil in a Hormuz-closure scenario, the operating costs of glass manufacturers rise substantially. This cost pressure eventually flows through to glass container prices, affecting the beverage, food, and pharmaceutical industries that rely on glass as a premium or safety-critical packaging format.

6. The Freight and Logistics Cascade

Even if a packaging converter has secured its raw materials ahead of a disruption, it faces an equally punishing challenge on the logistics side. The Strait of Hormuz closure is not just an oil story — it is a container shipping story.

Approximately 10% of the global container fleet was reportedly trapped inside the Gulf as the crisis deepened, and major carriers — MSC, CMA CGM, Hapag-Lloyd, and Maersk — halted or severely restricted services to Gulf ports including Jebel Ali (Dubai), Khalifa Port (Abu Dhabi), and Dammam (Saudi Arabia). These ports serve not only as destinations for goods consumed in the Gulf region but as critical transshipment hubs for cargo moving between Asia, the Middle East, Africa, and Europe. When they become inaccessible, the knock-on effects spread rapidly through global container networks.

For packaging supply chains, the freight cost impact operates through multiple simultaneous mechanisms that compound on each other. War Risk Surcharges of $1,500–$3,500 per TEU are the most visible, but they sit on top of Bunker Adjustment Factors driven by rising fuel costs, congestion surcharges at alternative transshipment ports like Colombo, Singapore, and Salalah, and potential peak-season premiums as carriers reposition capacity globally. As one logistics analysis noted, “when three or four independent surcharges compound simultaneously, total per-container costs can spike 30–50% above contracted base rates”. For packaging businesses operating on margins of 5–15%, a 30–50% spike in freight costs is not an inconvenience — it is an existential threat to contract profitability.

The rerouting of vessels around the Cape of Good Hope, already the default for traffic that would normally pass through Suez or Hormuz, adds approximately two weeks to transit times across the Asia-Europe corridor. For packaging materials manufactured in Asia — which is where the majority of the world’s plastic films, flexible packaging, and corrugated containerboard are produced — this means that inventory pipelines globally face a 10–14-day elongation almost immediately. Just-in-time supply chains, already stretched thin after years of lean inventory discipline and post-pandemic rationalization, are not designed to absorb this kind of shock without disruption.

7. Regional Vulnerabilities: Who Gets Hit Hardest?

The geographic distribution of packaging supply chain exposure to the Hormuz closure is uneven, but no major producing or consuming region escapes entirely unscathed.

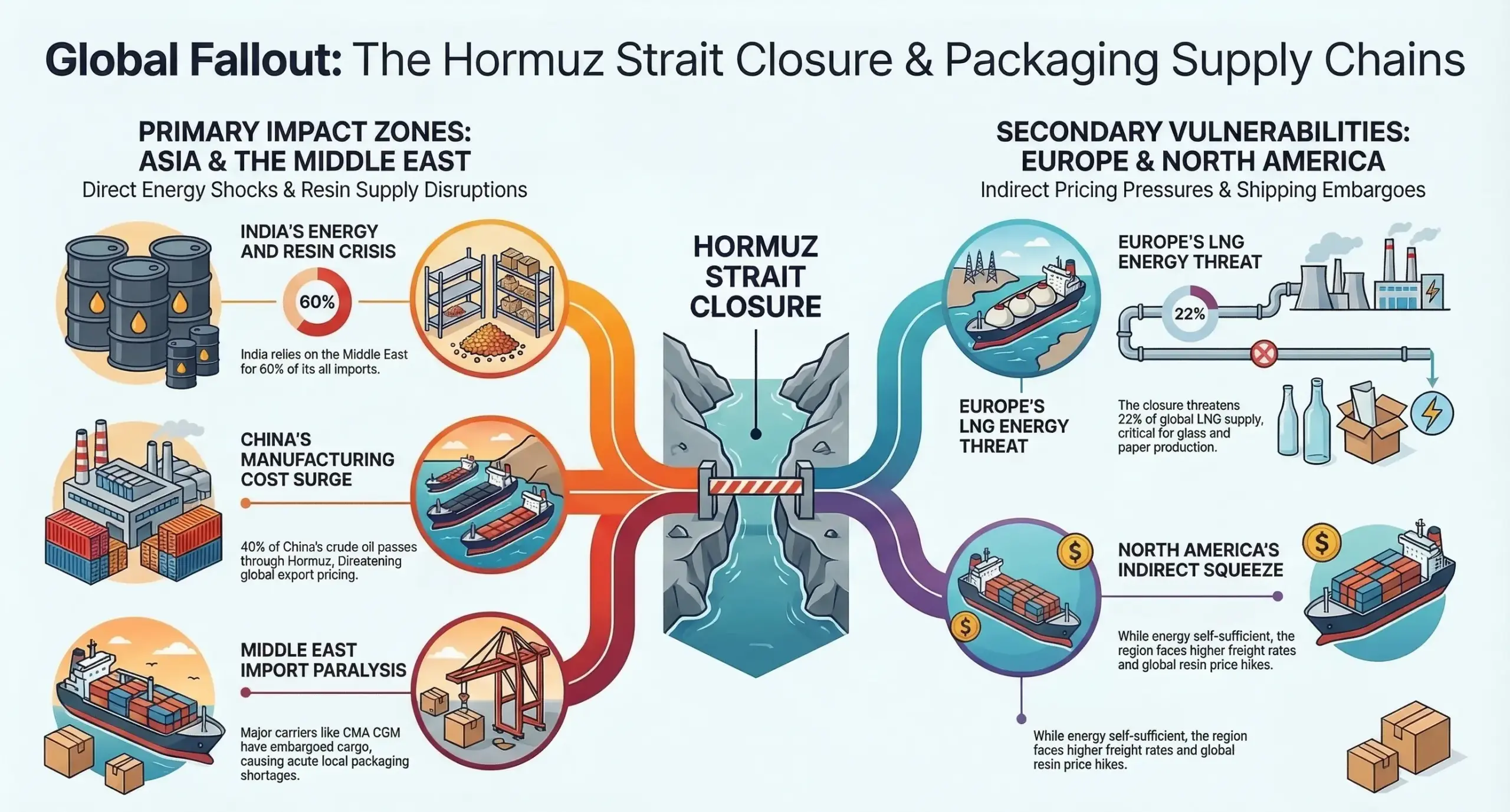

Asia bears the heaviest burden. India, with over 60% of its oil imports originating from the Middle East and a rapidly growing packaging sector driven by e-commerce and consumer goods demand, faces both the highest energy cost shock and the greatest supply chain disruption. South Korea, Thailand, and the Philippines are similarly exposed, being large consumers of imported petrochemical resins and packaging materials. China, the world’s largest crude oil importer, acquires roughly 40% of its oil through Hormuz, and any sustained disruption would raise the cost structure of its vast plastics and packaging manufacturing complex, putting pressure on export pricing globally.

Europe faces a different but serious set of vulnerabilities. European packaging manufacturers are not primarily sourcing resin from the Gulf, but they are heavy consumers of LNG for energy — and the closure of Hormuz threatens roughly 22% of global LNG supply. Energy-intensive industries, including glass and paper packaging, would see operating costs escalate significantly if LNG prices revisit the record highs of 2022, as some analysts now fear is possible. European pulp exporters sending material to Asian paper mills also face higher shipping costs.

The Middle East itself is both a major packaging production hub and a consumer market uniquely exposed to import disruption. Countries like the UAE, Qatar, Saudi Arabia, and Kuwait import vast quantities of finished packaging materials and machinery. The embargo placed by CMA CGM and Hapag-Lloyd on cargo to Gulf ports means that these imports are simply not moving for the duration of the crisis. Food, pharmaceutical, and consumer goods companies operating in the GCC region are facing acute shortages of packaging materials that normally arrive by container ship through Jebel Ali.

North America is the least directly exposed, given its relative energy self-sufficiency and the fact that its major packaging supply chains are served by North American and Latin American petrochemical producers. However, the indirect effects — through global resin price increases, higher freight rates on all trade lanes as capacity is absorbed by longer voyages, and supply tightness for specialty packaging materials sourced from Asia or Europe — will still be felt.

8. The Spectre of Inventory Depletion and Demand Shock

One dimension of the Hormuz closure that packaging professionals must plan for is the speed at which inventory buffers will be depleted. After years of lean supply chain management, many packaging buyers carry 4–8 weeks of inventory at most. In a disruption that adds two weeks to transit times while simultaneously tightening feedstock supply and raising resin prices, those buffers erode rapidly.

The experience of the Red Sea crisis in 2024 is instructive. When Houthi attacks in 2024 forced widespread rerouting of container vessels around the Cape of Good Hope — effectively removing roughly half the normal Suez Canal traffic — packaging supply chains in Europe and North America experienced meaningful lead time extensions, spot price spikes, and a wave of panic buying that further tightened availability. The Hormuz closure of 2026 is, by most measures, more severe: it affects a larger share of global oil trade, involves more trapped container capacity, and coincides with a feedstock cost shock that the Red Sea crisis did not deliver.

The Institute for Supply Management (ISM) has identified the Hormuz closure as a tri-level threat to manufacturing supply chains: first, through dependencies on petrochemical byproducts produced in or shipped through the Gulf; second, through the rerouting impact on all vessels traveling around Africa; and third, through the broader capacity implications of longer vessel voyages for the global container fleet. For packaging specifically, all three of these threats are active simultaneously.

9. Strategic Responses: What the Industry Is Doing

Faced with this multi-vector threat, packaging companies and their procurement teams are deploying a range of strategies to manage exposure and protect continuity.

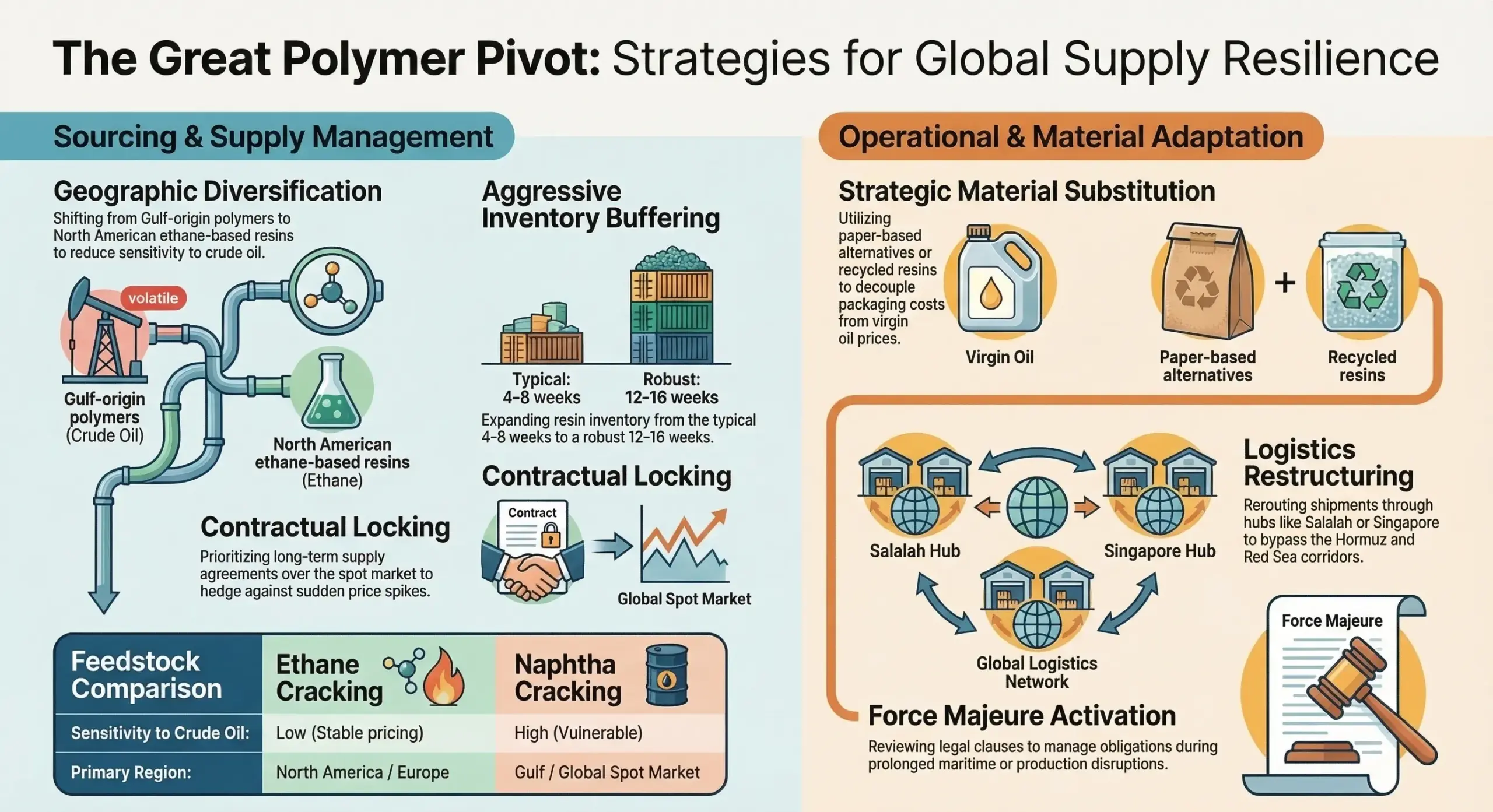

Geographic diversification of feedstock sourcing is the first and most obvious response. Companies heavily reliant on Gulf-origin polymers are accelerating conversations with North American and European resin producers — particularly those using ethane cracking, which is less sensitive to crude oil prices than naphtha-based cracking. U.S. ethane crackers in particular benefit from relatively stable natural gas liquids pricing that is partially decoupled from crude oil markets, offering a potential hedge.

Inventory building and forward buying are being activated wherever balance sheet capacity allows. Packaging converters and brand owners who can afford to accumulate 12–16 weeks of resin or substrate inventory — rather than the lean 4–8 weeks typical in normal times — are doing so, accepting the working capital cost in exchange for supply certainty.

Material substitution is gaining renewed attention. In flexible packaging, there has been growing interest in paper-based alternatives to plastic films for certain applications — ironic given that paper faces its own supply chain pressures, but the reduced oil-price sensitivity of paper is attractive in a crude-shock environment. Similarly, some packaging designers are revisiting the economics of recycled polymer resins, which carry price dynamics that can diverge from virgin resin markets when crude oil spikes.

Logistics restructuring is a more complex but urgent priority. Packaging companies are working with freight forwarders to identify the fastest and most cost-effective rerouting options for shipments that normally transit through Hormuz or the Suez/Red Sea corridor. Transshipment through Salalah (Oman), Colombo (Sri Lanka), or Singapore as alternative hubs can recover some lead time lost to Cape of Good Hope rerouting, though these ports are now facing congestion surcharges of their own.

Contract review and force majeure clauses are being dusted off across the industry. The Hormuz closure constitutes a qualifying event under most standard force majeure provisions, and both suppliers and buyers are examining their contractual obligations in the context of a potentially prolonged disruption. Companies that locked in long-term resin supply agreements at pre-crisis prices are now in a vastly stronger position than those buying on the spot market.

10. The Long Shadow: Structural Implications for Packaging

If the Hormuz disruption proves sustained — lasting weeks or months rather than days — it will accelerate structural shifts in the packaging supply chain that were already underway before the first shot was fired.

The first of these is the regionalization of supply chains. The COVID-19 pandemic initiated a broad rethinking of globally extended, single-source supply chains. The Red Sea crisis of 2024 reinforced it. The Hormuz closure of 2026 is delivering what may be the definitive argument for regional self-sufficiency in packaging materials. Companies and governments alike are likely to accelerate investment in domestic or near-shore petrochemical capacity, reducing dependence on Gulf feedstocks and global container shipping.

The second structural shift is the acceleration of circular economy and recycled content adoption. Every oil price shock since the 1970s has ultimately created some degree of demand destruction for virgin plastics, boosting the relative economics of recycled materials. With recycled polymer prices partially decoupled from crude oil, a sustained crude spike makes recycled PE, PP, and PET more cost-competitive relative to their virgin equivalents than in any environment of cheap oil. Brands and converters that have been building recycled content capability will find that capability suddenly very valuable.

The third shift is toward increased packaging efficiency and material reduction. When resin costs spike by 20–40%, the return on investment for lightweighting programs — reducing the gauge of plastic film, thinning container walls, eliminating unnecessary layers in laminates — improves dramatically. The current crisis is likely to accelerate investments in packaging design optimization that reduce total material consumption and, therefore, exposure to feedstock price volatility.

11. Conclusion: A Chokepoint for More Than Oil

The Strait of Hormuz has always been understood as a chokepoint for oil. What the events of early March 2026 are making viscerally clear is that it is equally a chokepoint for the modern packaging supply chain. From the naphtha that becomes PE film, to the LNG that powers paper mills and glass furnaces, to the container ships that carry packaging materials from factories in Asia to consumers across the world, the 33 kilometers of the Strait function as an invisible link in every supply chain that relies on plastic wrap, a cardboard box, an aluminum can, or a glass bottle.

The industry’s response will ultimately be shaped by how long the disruption persists. A closure of days creates manageable cost shocks that can be absorbed or passed on. A closure of weeks creates genuine feedstock shortages, empties resin inventory buffers, and forces structural contract renegotiations. A closure of months fundamentally re-draws the map of global packaging supply chains, accelerating the regionalization, decarbonization, and circular economy trends that have been building for years.

What is not in question is the vulnerability that this crisis has exposed. A packaging industry that sources the majority of its raw materials from petrochemical complexes served by a single maritime chokepoint, and ships finished goods through container networks where 10% of the global fleet can be suddenly trapped, has a concentration risk that no amount of efficiency optimization can fully mitigate. The Strait of Hormuz is not just a waterway. For the global packaging supply chain, it is the thinnest thread from which a very large and very complex system is hanging.

FAQs

Which packaging materials are most directly impacted by the closure?

Plastic packaging is the most immediately and severely impacted category. Around 80% of Asia’s seaborne naphtha import demand is covered by Middle Eastern supply, and naphtha is the key feedstock for ethylene and propylene production in Asia and Europe. When that supply is disrupted, the cost and availability of PE, PP, PET, and PVC all come under pressure. European PE/PP producers have already moved from seeking modest price increases of €30–50 per tonne for March contracts to proposing triple-digit increases. Aluminum packaging faces disruption because Middle Eastern smelters are trapped behind the closure and War Risk Surcharges add roughly $75 per tonne to shipping costs. Glass and paper packaging are hit indirectly through surging energy costs, as European natural gas prices rocketed 50% after QatarEnergy halted LNG production at Ras Laffan due to conflict-related attacks.

How much are freight costs rising for packaging companies?

Freight costs are rising sharply through a combination of simultaneously compounding surcharges. Hapag-Lloyd imposed a War Risk Surcharge (WRS) of $1,500 per standard TEU and $3,500 per reefer container for all Gulf-related cargo as of early March 2026. These surcharges stack on top of Bunker Adjustment Factors (driven by rising fuel costs), congestion surcharges at alternative transshipment ports, and potential capacity premiums as the global fleet is stretched by longer rerouted voyages. When these surcharges compound simultaneously, total per-container costs can spike 30–50% above contracted base rates. For packaging businesses operating on typical margins of 5–15%, a freight cost surge of this magnitude is an existential threat to contract profitability rather than a manageable inconvenience.

How does the closure affect resin and polymer prices specifically?

The price transmission mechanism is rapid and mechanical. When crude oil rises, naphtha becomes more expensive; when naphtha rises, the cost of steam-cracking ethylene and propylene increases; and when those olefins spike, PE, PP, PET, and PVC resin prices follow. ICIS director of Energy & Refining Ajay Parmar forecasted Brent crude rising sharply to around $90 per barrel in March as the market prices both disruption risk and constrained physical flows from the Gulf. Propylene margins face added compression because disruptions to Middle East propane supply raise feedstock costs for propane dehydrogenation (PDH) units, according to ICIS senior analyst Joey Zhou. Meanwhile, U.S. ethylene glycol (EG) prices are expected to rise in the short term as Asian spot prices increase and demand for U.S. exports grows to compensate for the loss of Gulf supply.

Are there alternative supply routes for petrochemicals and packaging feedstocks?

Some partial alternatives exist, but none can fully compensate for the closure. Saudi Arabia’s Petroline pipeline can carry up to 5 million barrels per day to Red Sea terminals, and the UAE has the Abu Dhabi Crude Oil Pipeline (ADCOP) capable of roughly 1.5 million barrels per day to Fujairah — but together these offset only a fraction of the roughly 13 million barrels per day that normally transit the Strait. For LNG, there is no pipeline alternative whatsoever. On the chemicals and resins side, SABIC’s Yanbu plants on Saudi Arabia’s west coast may partially bypass the Strait by exporting via the Red Sea — but the Red Sea itself remains a risk zone due to ongoing Houthi threats, making this a precarious workaround. U.S. producers of olefins and polyolefins using shale gas feedstock will become more cost-advantaged on a relative basis as crude rises, but a “complete switch from existing Middle Eastern supply chains is not something that happens overnight,” as one ICIS analyst noted.

Which regions and packaging markets are hit hardest?

Asia bears the heaviest burden. India sources over 60% of its oil imports from the Middle East, and countries like South Korea, Thailand, and the Philippines are major consumers of imported petrochemical resins. China, the world’s largest packaging producer, acquires roughly 40% of its crude through Hormuz. Europe is exposed primarily through LNG prices — the 50% spike in European natural gas prices following QatarEnergy’s Ras Laffan shutdown translates directly into higher operating costs for glass, paper, and plastics manufacturing. The Middle East itself faces acute packaging import shortages, as carriers like CMA CGM and Hapag-Lloyd have embargoed Gulf ports including Jebel Ali, Khalifa Port, and Dammam. North America is the least directly exposed due to domestic energy production, but will still feel the effects through global resin price inflation and tighter container capacity worldwide.

How long could the disruption last, and does duration matter for packaging?

Duration matters enormously for the severity of the supply chain impact. A closure of days creates manageable cost shocks that can be absorbed through existing inventory buffers. A closure of weeks — which the current situation appears to be — begins depleting the 4–8 week resin and substrate inventories that most packaging buyers carry under lean supply chain practices, while simultaneously elongating lead times by two or more weeks through Cape of Good Hope rerouting. A closure of months would fundamentally redraw global packaging supply chains, force structural contract renegotiations, and potentially cause physical feedstock shortages at cracking facilities that cannot be resolved simply by paying a higher price. ICIS analysis assumes the conflict continues through at least March 2026 and that the Strait remains “unofficially restricted in the near term”.